The current American macroeconomic landscape has placed digital entrepreneurs and remote workers under unprecedented pressure. With total U.S. household debt hovering around a historic $18.8 trillion, navigating high revolving balances requires an analytical, systematic framework rather than generic advice. Stubborn inflationary pressures on baseline necessities like housing, insurance, and utilities mean that traditional budgeting advice no longer cuts it. If you want to scale your business or unlock true remote freedom, learning how to get out of debt fast in the USA is the foundational step to reclaiming your financial sovereignty.

Table of Contents

The Core Blueprints Section

When executing an aggressive debt payoff strategy, two main operational methodologies dominate the space. Both require you to maintain absolute consistency by paying the minimum required balances on all accounts while routing every single dollar of your surplus monthly income toward a single target asset.

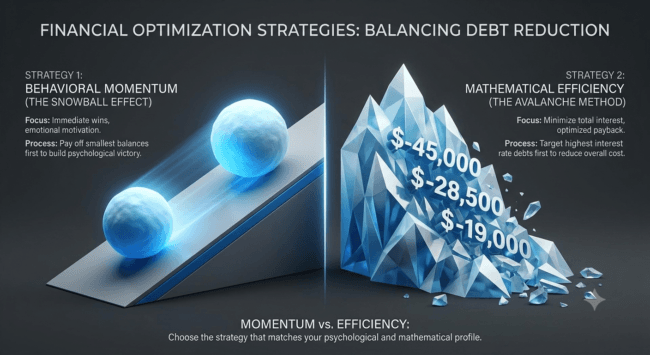

The Debt Snowball Methodology

- Operational Mechanism: Order your outstanding liabilities strictly from the lowest face value balance to the highest, completely ignoring the corresponding annual percentage rates (APRs).

- Psychological Advantage: Clearing out smaller balances rapidly creates immediate behavioral wins, releasing dopamine and reinforcing structural habit changes.

- Target Demographics: Best suited for individuals who experience execution fatigue or feel emotionally overwhelmed by a high volume of individual open accounts.

The Debt Avalanche Methodology

- Operational Mechanism: Sort every item on your liability sheet based strictly on interest rates, prioritizing the highest APR account regardless of the nominal balance.

- Mathematical Advantage: Minimizes compounding interest leakage over time, ensuring that fewer total dollars leave your ecosystem.

- Target Demographics: Mathematically optimal for hyper-rational operators, spreadsheet-driven freelancers, and entrepreneurs with massive, high-interest commercial credit lines.

The Technical Execution Section

To systematically implement your chosen strategy, you need to rely on digital automation rather than manual willpower. Tracking your numbers via an AI-driven financial planning tool or a structured, automated spreadsheet ensures zero execution friction.

Step 1: Centralizing and Sanitizing Your Liabilities

Before executing either strategy, you must aggregate your financial data. Extract every open liability across your accounts, ensuring you document the exact current balance, current APR, and absolute minimum payment down to the penny.

Step 2: Selecting and Deploying Your Payoff Engine

To run these numbers without human error, you can use interactive software models. Below is an embedded, production-grade automated engine designed to calculate your exact optimization paths without requiring external accounts or manual math.

2026 Strategy Path Matrix Optimizer

Live EngineChange the values below to see how injecting extra cash flow from digital side hustles accelerates your path to absolute financial freedom.

Total Months to Financial Freedom with Extra Income: —

Step 3: Setting Up Platform Automation and API Bridges

- Establish Secure Financial Data Feeds: Link your primary business checking accounts to a centralized budgeting app using secure financial APIs. This allows your live transaction records to sync automatically without manual entries.

- Configure Fixed Minimum Autopay: Log into each underlying creditor platform and schedule automatic recurring payments for the exact minimum amount due, timed precisely two days after your primary revenue processing cycle.

- Deploy Capital Routing Automation: Program your primary checking account to automatically transfer your calculated surplus monthly cash directly to your target debt account via an automated recurring ACH transfer. This completely removes human hesitation from your wealth building engine.

Funding Your Strategy: Monetizing Your Free Time

When trying to figure out how to get out of debt fast in the USA, optimizing your current budget is only half the battle. To drastically speed up either the debt snowball vs avalanche method, you must attack the problem from both sides by aggressively driving up your monthly revenue. The fastest way to unlock an extra $500 to $2,000 per month specifically to throw at your principal balances is by deploying remote digital side hustles.

By leveraging remote freelance opportunities—such as online transcription roles, high-ticket virtual assistant services, or targeted affiliate marketing—you can generate dedicated income streams that go straight toward eliminating your debt. Instead of letting your day job income carry the entire load, setting up a secondary, internet-based income engine ensures that your debt repayment timeline shrinks from years down to months.

Unfiltered Podcast Q&A Style Framework

How can I learn how to get out of debt fast in the USA?

To master how to get out of debt fast in the USA, you must immediately freeze all new credit utilization, construct a rigorous cash-flow balance sheet, and deploy every single dollar of non-essential income toward your priority liability using either the snowball or avalanche framework.

Which system wins when evaluating the debt snowball vs avalanche method?

When choosing between the debt snowball vs avalanche method, the avalanche method wins on raw mathematical efficiency by saving money on compounding interest, whereas the snowball method wins on behavioral execution by delivering fast, actionable milestones.

What do current U.S. consumer debt statistics 2026 indicate about credit card usage?

The newest U.S. consumer debt statistics 2026 reveal that revolving credit card balances have ballooned past a record $1.21 trillion, showing a structural reliance on plastic amid sticky living costs.

How can I integrate AI-driven financial planning tools into my recovery plan?

You can use AI-driven financial planning tools to automatically parse your historical transactional CSV files, categorize waste patterns, and run predictive cash-flow forecasting algorithms.

When should someone consider debt consolidation interest rate optimization?

You should pursue debt consolidation interest rate optimization the moment your weighted average interest rate across your credit lines climbs higher than the fixed APR of an uncollateralized personal consolidation loan or a 0% balance transfer promotion.

How does a high debt-to-income ratio damage a remote worker's mortgage application?

A sky-high debt-to-income ratio acts as an instant red flag for automated underwriter algorithms, signaling that a significant portion of your monthly income is locked into servicing old obligations.

Why do balance transfer credit cards function as a double-edged sword?

Utilizing a balance transfer credit card can temporarily freeze interest accumulation for up to 21 months, but if you fail to wipe out the principal before the promotional window slams shut, you run into punitive retroactive interest schedules.

What is the underlying danger of utilizing automated payday advance apps?

Frequent use of automated payday advance apps traps users in a predatory cash-flow loop, masking structural income shortfalls with high hidden administrative service fees.

How can an emergency fund buffer prevent relapsing into high-interest debt?

Maintaining a liquid emergency fund buffer of three to six months of bare-minimum operational expenses prevents unexpected financial emergencies from blowing up your repayment velocity.

What structural traps exist within traditional credit counseling services?

Many legacy credit counseling services claim to be non-profit organizations, yet they frequently sneak in mandatory monthly administration fees that drain the capital you could use to pay down your balances.

How does the snowball method protect you from cognitive overload?

The systematic setup of the snowball method reduces cognitive overload by reducing the total number of moving financial parts you have to track down to a bare minimum.

Can an algorithmic budget template outpace a human financial planner?

An optimized algorithmic budget template provides unbiased math and instant updates, making it far cheaper and more agile than a traditional human advisor for early-stage debt management.

Why is relying entirely on liquid cash reserves a mistake during hyper-inflation?

Holding large liquid cash reserves during inflationary cycles erodes your purchasing power, meaning that surplus cash is often better spent wiping out guaranteed 20%+ toxic interest debt.

How can digital freelancers protect their cash flow from variable income drops?

Freelancers must utilize a variable income buffer system, holding back surplus revenue from peak billing months in a dedicated account to cover fixed debt payments during dry seasons.

What is the financial impact of strategic credit score optimization during debt payoff?

Maintaining a clean credit score optimization routine while aggressively paying down principal allows you to qualify for premium refinancing terms halfway through your journey.

How can I use side hustle revenue generation to speed up my progress?

Directing 100% of your side hustle revenue generation toward your priority accounts bypasses your day-to-day lifestyle budget, immediately cutting down your repayment timeline.

Why do peer-to-peer lending networks offer an alternative to traditional commercial banks?

Vetted peer-to-peer lending networks cut out institutional middlemen, allowing borrowers with solid credit history to source lower interest capital funded directly by individual retail investors.

What happens behind closed doors during a debt settlement negotiation?

Initiating a formal debt settlement negotiation requires you to intentionally default on payments, which drops your credit profile before the bank agrees to write off a portion of your principal.

How do modern budgeting apps use behavioral psychology to curb overspending?

The design of modern budgeting apps uses instant push notifications and visual charts to introduce positive friction whenever your spending approaches predefined limits.

Why should you avoid tapping into your employer-sponsored 401k account for debt relief?

Taking an early employer-sponsored 401k loan strips your retirement capital of compounding growth potential and triggers immediate tax penalties if you leave your job.

How can a zero-based budgeting framework optimize every incoming dollar?

Implementing a zero-based budgeting framework forces you to give every single dollar a job before the month begins, ensuring your surplus cash doesn't get spent on lifestyle creep.

What are the real risks of using home equity lines of credit to pay off credit cards?

Converting unsecured debt into a home equity line of credit lowers your interest rate, but it moves the risk onto your primary residence, leaving you open to foreclosure if your income drops.

How can remote workers maximize geographic arbitrage to accelerate their payoff?

Practicing smart geographic arbitrage allows digital professionals to earn in strong currencies like USD while living in low-cost-of-living regions to hyper-optimize their savings rate.

What are the long-term consequences of public record bankruptcy chapters?

Filing for legal public record bankruptcy offers a structural reset, but it leaves a major mark on your credit history for up to ten years, making future business borrowing incredibly expensive.

Why do automatic micro-saving apps often fail to move the needle on deep debt?

Relying on automatic micro-saving apps that round up your coffee purchases provides a false sense of accomplishment without contributing the serious capital needed to wipe out large debts.

How does negotiating directly with original creditors change your financial trajectory?

Securing a direct hardship program agreement with your original bank can lower your APR down to single digits for a fixed period without destroying your credit profile.

Why are high-yield savings accounts secondary to paying off double-digit toxic debt?

An elite high-yield savings account yields around 4-5% annual returns, which pales in comparison to the guaranteed 20-30% return you get by wiping out high-interest credit card debt.

How can an automated net worth dashboard keep you motivated over time?

Using an automated net worth dashboard turns your financial recovery into a game, shifting your focus from your heavy liabilities to your growing net worth.

What hidden dangers lie within buy now pay later financing models?

The explosive growth of buy now pay later financing splits up small retail purchases into seemingly harmless fragments that can quietly derail your monthly cash-flow budget.

How can you protect your lifestyle from extreme frugality burnout?

To avoid extreme frugality burnout, your budget must include a small, fixed allocation for guilt-free personal spending to make your long-term plan sustainable.

What is the fastest way to drop your credit card utilization ratio?

Making strategic mid-cycle statement payments before the official monthly reporting date lowers your reported utilization, instantly boosting your credit score.

Structural Enhancements

Dynamic Performance Comparison Table

| Technical Metric | The Debt Snowball Strategy | The Debt Avalanche Strategy |

| Algorithmic Prioritization Metric | Nominal Balance Face Value (Smallest to Largest) | Annual Percentage Rate / APR (Highest to Lowest) |

| Total Lifetime Interest Leakage | Suboptimal (Higher interest lines run longer) | Mathematically Optimized (Minimizes aggregate interest) |

| Velocity to First Account Liquidation | Fast (Clears micro-balances within 30–90 days) | Variable (Can take months if the highest APR balance is massive) |

| Required Behavioral Discipline | Moderate (Fueled by frequent psychological wins) | High (Requires tracking cold numbers without early wins) |

| True Financial Efficiency Rating | Sub-Optimal | Maximum Efficiency |

The "Ugly Truth" Section

Let's cut through the polished financial marketing. A deep dive into actual user experiences on Reddit (r/personalfinance) and Trustpilot reveals that both strategies often look better on paper than they play out in real life.

The biggest pitfall isn't the math; it's systemic fatigue and predatory creditor behavior. Real-world users frequently complain about a phenomenon known as "balance chasing." This happens when an algorithm at a major bank sees you making massive principal payments and instantly slashes your overall credit limit to match your new, lower balance. This predatory move ruins your credit utilization ratio overnight, despite your hard work.

Furthermore, avalanche purists on Reddit report throwing in the towel around month four because tackling a massive $20,000 balance at 29% APR feels like trying to empty the ocean with a spoon. Snowball users face the opposite trap, looking back after two years only to realize they sacrificed thousands of dollars in extra interest leakage just for a few early psychological wins.

Step-by-Step Launch Summary Checklist

- [ ] Download the last six months of all credit card, personal loan, and business statements to map out your true liabilities.

- [ ] Extract and input your balances, APRs, and minimum payments into your centralized tracking engine.

- [ ] Choose your strategic path: select the Snowball method for quick behavioral wins or the Avalanche method for maximum interest savings.

- [ ] Configure your primary checking account to automate the minimum payments across all open accounts.

- [ ] Audit your monthly subscriptions and cut non-essential expenses to find at least $250 in extra cash.

- [ ] Set up an extra income stream via digital side hustles to actively feed your capital pool.

- [ ] Route your automated surplus cash toward your top-priority account.

- [ ] Set up an automated monthly review to track your progress and adjust your strategy if your income changes.

Internal and External Linking Placeholders

- Virtual Bookkeeping Business 2026 USA

- How to Make Money with Airbnb in 2026 USA Without Owning Property

- Best Work From Home Jobs for Introverts in the USA 2026 (No Phone, No Sales)

- Zero-Based Budgeting 2026 USA

- Best Budgeting Apps USA 2026

- Highest Paying Gig Economy Jobs in the USA 2026

- How to Start a Notion Template Business in 2026 USA

- Freelance Digital Skills That Pay 2026 USA

- Best Budgeting Tips for 2026 in USA

- Voiceover Jobs 2026 USA

- Virtual Bookkeeping Business 2026 USA

- Proofreading Jobs Online 2026 USA

- AI Data Annotation Jobs 2026 USA

- Online Transcription Jobs 2026 USA

- User Testing Jobs 2026 USA

- How to Become an AI Prompt Engineer in 2026 USA

- Best Secret Remote Job Boards 2026 USA

- Upwork for Beginners in 2026 USA

- Pinterest Affiliate Marketing in 2026 USA

- How to Start a Faceless YouTube Channel in 2026 USA

- How to Start Amazon KDP in 2026 USA

- How to Start Dropshipping in 2026 USA

- How to Create and Sell Online Courses in 2026 USA

- External Reference Link 1: — Consumer Financial Protection Bureau Bureau Updates on Credit Regulations]

- External Reference Link 2: — Federal Reserve Bank of New York Household Debt and Credit Report]

Compliant Income Disclaimers

Regulatory Notice & Financial Disclaimer: Your individual financial results may vary based on your personal situation. The operational frameworks, calculations, and strategies discussed in this article are designed solely for educational and informational purposes. This content does not constitute formal investment, legal, or licensed financial planning advice. Debt reduction timelines depend heavily on individual income consistency, creditor policies, and wider economic conditions.

Short FAQ Block

- What happens if a creditor suddenly closes my account after I pay it off?This is a common practice known as balance chasing. When banks see high credit risk across the board, they often cut your credit limit down to match your new balance as you pay it off. This can temporarily spike your credit utilization ratio, but you can offset it by keeping your focus on reducing your overall principal.

- Should I stop contributing to my company 401k match while paying down debt?Never leave free money on the table. If your employer offers a matching 401k contribution, invest just enough to secure the full match. The immediate return on a company match almost always beats the interest you would save by routing that cash toward your debt. Once you secure the match, send every remaining dollar toward your debt payoff.

- How do I handle unpredictable expenses while running a tight debt payoff plan?To protect your plan, build a small starter emergency fund of $1,000 to $1,500 before launching your snowball or avalanche strategy. This baseline fund acts as a buffer, ensuring that unexpected car repairs or medical bills don't force you to take on new credit and break your momentum.