Let’s cut through the noise. Most personal finance advice online was written when rent was half what it costs today, gas didn’t feel like a luxury, and “inflation” was just an economic textbook term. It’s 2026, and the economic ground under American households has fundamentally shifted. According to recent data from the Bureau of Labor Statistics (BLS), core consumer prices and shelter spikes have forced the average American household to spend over 44% of their net income purely on non-discretionary survival needs.

Grocery bills are up. Rent in major metros is punishing. And yet — the foundational principle behind the 50/30/20 budget rule 2026 hasn’t just survived. When applied with software-driven intelligence, it remains the most actionable financial framework the average American can deploy right now to consistently save $500 to $1,000 per month.

This isn’t a motivational post. This is an operational, technical breakdown built for remote workers, gig economy earners, dual-income households, and solo entrepreneurs who need a cash architecture that actually fits 2026 macroeconomic realities.

Table of Contents

The Core Blueprints Section

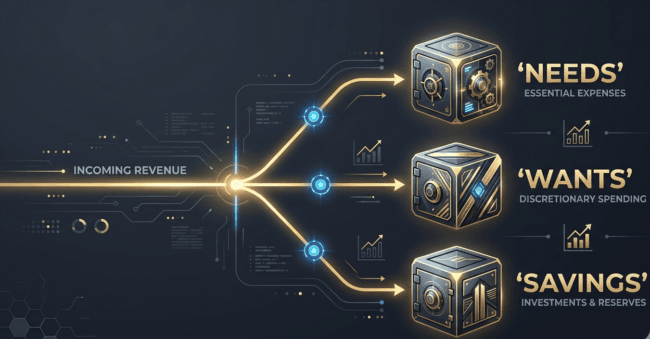

Originally popularized by Senator Elizabeth Warren, the core formula of this allocation strategy splits your net income into three distinct macro-allocated operational zones. But in 2026, with the median household income hovering around $78,000 and average rent in growth hubs like Austin, Denver, and Raleigh crossing $1,800/month for a one-bedroom, these buckets require precise redefinition.

- 50% Allocation — Non-Negotiable Fixed Needs: These are your absolute survival costs. Cut them, and your life stops functioning. This includes rent or mortgage commitments, utility infrastructure (electric, water, essential broadband), base groceries, healthcare premiums, and minimum structural debt payments (student loans, auto notes). 2026 Calibration: If your rent alone exceeds 35% of your take-home pay, the 50% ceiling is heavily breached before you buy food. You must use tactical software systems to monitor this leak.

- 30% Allocation — Lifestyle & Discretionary Wants: Wants are your variable lifestyle layer. They span streaming networks (Netflix, Hulu, Apple One), delivery apps, gym memberships, hobbies, and non-essential travel. Investigator’s Note: The average American household now spends a staggering $219/month purely on automated subscriptions—this hidden drain is exactly where your potential $1,000 monthly savings vanishes.

- 20% Allocation — Future Financial Capital Accumulation: This baseline drives long-term wealth creation and risk mitigation. It splits immediately between liquid emergency cash parked in High-Yield Savings Accounts (HYSA), automated index fund investments, and aggressive principal debt reduction beyond the minimum requirements.

The Technical Execution Section

To convert this financial theory into an automated, working pipeline, you must implement modern financial tracking systems for Americans. Relying on manual willpower fails; you need to build software-driven workflows that route cash automatically before you can spend it.

Step 1: Calculate Your True After-Tax Monthly Income

Do not use your gross salary. Do not use your W-2. Use your net deposit — what actually hits your checking account each pay period.

- Salaried employees: Take your bi-weekly or semi-monthly net deposit and multiply accordingly (×2 for semi-monthly; ×26÷12 for bi-weekly = ×2.167).

- Freelancers & gig workers: Average your last 3–6 months of net deposits. Then subtract your estimated quarterly self-employment tax liability (roughly 25–30% of gross for most SE earners). Use that number as your base.

Step 2: Account Structuring and API Handshakes

- Open Separate Vaults: Open a primary checking account (Needs Hub) and a secondary checking account (Wants Hub) at an agile digital institution like Ally Bank, SoFi, or Wealthfront. Link these directly to an isolated HYSA paying 4.5% to 5.2% APY (like Marcus or wealth portals) dedicated solely to the 20% savings bucket.

- Plaid Authorization: Inside your tracking software dashboard (Monarch Money or Copilot), navigate to

Settings > Connected Accounts > Add Account. Authenticate your core banking institutions via the secure Plaid API handshake to enable automated automated personal finance workflows. - Freelance Tax Withholding: For independent digital creators, execute an automated rule: sweep 25-30% of gross incoming invoice receipts into a separate tax holding vault before computing the net baseline for your personal allocations.

Step 3: Connect Third-Party Automation Tools via API Sweep Rules

To completely eliminate human friction, configure automated sweep rules within your bank’s bill-pay system to distribute your net funds exactly 24 hours after your income deposit hits:

- Payday Deposit ──> Goes to Primary Checking (Needs Hub)

- Auto-Transfer 30% ──> Sweeps to Secondary Checking (Wants Hub)

- Auto-Transfer 20% ──> Sweeps to HYSA / Brokerage Vault

When your Wants checking account hits zero, discretionary spending stops automatically for the month. No exceptions.

Step 4: Adjusting for High Cost-of-Living (COL) Environments

If you live in a punishing market like San Francisco, New York, or Los Angeles, the standard 50% needs bucket is mathematically insufficient due to real estate hyper-inflation. You must deploy the Modified 60/20/20 Rule: Allocate 60% to Needs, slash your Wants strictly to 20%, and hold the line at 20% for Savings. Keep active tabs on [Best Work From Home Jobs for Introverts in the USA 2026] to bridge this housing gap by scaling your top-line revenue.

Unfiltered Podcast Q&A Style Framework

What is the exact formula for computing post tax net monthly income?

Post tax net monthly income is calculated by taking your gross revenue and subtracting local, state, and federal taxes, along with mandatory health premiums. This gives you the exact baseline dollar amount needed to initialize your macro-allocations under the 50/30/20 budget rule 2026 architecture.

How do freelance income budgeting strategies adapt to erratic payment cycles?

Deploying specialized freelance income budgeting strategies requires establishing a “buffer bucket” using a 90-day rolling average of your net earnings to smooth out low-revenue months.

Which automated personal finance workflows eliminate manual bookkeeping friction?

Setting up automated personal finance workflows through services like Zapier or native banking tools allows you to route cash to specific destination accounts the moment a deposit is cleared.

Why do AI driven envelope banking software platforms outperform static spreadsheets?

Modern AI driven envelope banking software uses predictive machine learning algorithms to automatically tag and sort dynamic transactions with up to 95% classification accuracy.

When should you scale personal capital allocations toward long term investments?

You can scale personal capital allocations toward index funds and brokerage accounts only after your liquid emergency fund holds at least six months of baseline living expenses.

How does rent tracking automation protect your baseline lifestyle overhead?

Utilizing rent tracking automation tools helps you monitor your fixed housing costs in real time, ensuring your primary lease doesn’t stealthily over-consume your 50% needs tranche.

What are the best inflation proof high yield savings accounts right now?

The most reliable inflation proof high yield savings accounts are digital banking vaults that offer automated interest sweeping and yield matching above the core Fed funds rate.

How do pre tax 401k contribution rules interact with net income distribution?

Maxing out your pre tax 401k contribution rules reduces your overall gross taxable base, meaning you calculate your 50/30/20 proportions from a smaller, optimized net amount.

Can extra debt principal reduction payments be classified under the savings tranche?

Aggressive debt principal reduction payments that go beyond your contractual minimums are technically capital optimizations, meaning they fit perfectly inside your 20% financial goals bucket.

What are the best remote worker home office tax deductions for digital entrepreneurs?

Claiming remote worker home office tax deductions requires measuring your dedicated workspace square footage to write off a proportional slice of your home utility and internet costs on Schedule C.

How do digital cash sub vaults help track short term leisure goals?

Configuring digital cash sub vaults inside your secondary checking account allows you to fund specific vacations or gear upgrades entirely out of your designated 30% lifestyle budget.

What should you do when fixed living expenses exceed half your income?

If your fixed living expenses naturally cross the 50% threshold, you must temporarily switch to a 70/20/10 structure while actively cutting recurring luxury overhead.

How do automatic debit system safeguards prevent impulsive retail spending?

Enabling strict automatic debit system safeguards moves your savings and bill money out of your main checking account on payday, physically limiting the cash available for impulse buys.

How do credit card cash back optimization strategies impact your monthly budget?

Treating credit card cash back optimization strategies as extra windfalls—rather than regular income—allows you to route those bonus points directly into your investment account.

Why is a monthly macro spending trend audit essential for freelancers?

Running a monthly macro spending trend audit prevents structural budget creep, allowing independent creators to adjust their lifestyle categories before cash leaks become severe.

Where should you store health savings account deductible capital for maximum protection?

Keeping your health savings account deductible capital parked inside an investment-linked HSA ensures your medical safety net grows tax-free while remaining completely liquid.

What is the fastest way to execute a subscription clearing optimization audit?

A complete subscription clearing optimization audit involves using apps like Rocket Money to flag hidden, recurring micro-charges and cancel them instantly with one click.

How should pet care expense classification be handled under a macro budget?

Standard pet care expense classification places predictable food and mandatory insurance premiums under your 50% needs, while gourmet treats and toys belong in the 30% wants column.

Can robotic process automation banking scripts accelerate your debt payoff?

Writing simple robotic process automation banking scripts lets you auto-transfer any leftover money in your checking account directly toward your highest-interest credit card balance at the end of the month.

How does the 50/30/20 budget rule 2026 adapt to high cost of living cities?

Surviving in a high cost of living city often means tweaking the framework to a 60/20/20 split, consciously lowering your lifestyle spending to balance out expensive urban rent.

Why are liquid capital cash reserves critical during sudden economic downturns?

Maintaining liquid capital cash reserves in a secure account prevents you from having to sell off your long-term stock investments at a loss when unexpected emergencies happen.

Should real estate down payment savings be mixed with emergency cash?

Building a real estate down payment savings pipeline requires creating a totally separate sub-account within your 20% allocation, keeping your core emergency money completely untouched.

How do split transaction ledger features handle mixed warehouse store receipts?

Using split transaction ledger features in finance apps allows you to break a single Costco receipt into base groceries (needs) and home electronics (wants).

What are the risks of high volatility asset investing within your savings bucket?

Relying too heavily on high volatility asset investing (like crypto or individual tech stocks) can leave your core 20% savings exposed to sudden market drops when you need cash the most.

How do independent contractor quarterly tax estimations protect your business cash flow?

Calculating accurate independent contractor quarterly tax estimations ensures you route 30% of every invoice straight into a hidden tax vault before calculating your take-home pay.

What is the fastest job loss financial rebalancing protocol to implement immediately?

Executing a job loss financial rebalancing protocol means freezing all 30% discretionary spending instantly and re-routing all automated workflows to protect your core lifestyle survival fund.

Is a boutique gym membership spending choice classified as a need or a want?

A luxury boutique gym membership spending choice is technically a lifestyle luxury that must be paid for out of your 30% wants allowance, unless it’s a doctor-prescribed medical cost.

How do annual insurance premium amortization strategies prevent sudden cash crunches?

Using annual insurance premium amortization strategies means dividing your big yearly bills by 12 and auto-saving that exact amount each month so you aren’t blindsided when the bill comes due.

Can dual income joint household budgeting systems use separate 50/30/20 tracks?

Running dual income joint household budgeting systems works best when both partners manage their own personal accounts while auto-transferring fixed percentages to a shared pool for bills.

What is the psychological value of an automated wealth accumulation system?

Building an automated wealth accumulation system takes the willpower out of saving, helping your net worth grow quietly in the background without constant stress or decision fatigue.

How do you eliminate payment platform digital transaction leakage?

Stopping payment platform digital transaction leakage requires auditing your Venmo, PayPal, and Apple Pay histories every 90 days to clear out forgotten micro-subscriptions and automatic app charges.

Structural Enhancements

Dynamic Performance Comparison Table

To evaluate how these automated strategies compare across core technical budgeting setups, review the framework matrix below:

| Budgeting Framework | Implementation Friction | Technical Automation Overhead | Behavioral Discipline Required | Multi-Income Scalability | Target Audience Match |

|---|---|---|---|---|---|

| 50/30/20 Macro Allocation | Low | Medium | Low | High | Digital Entrepreneurs / Remote Workers |

| Zero-Based Budgeting | High | High | High | Low | Fixed-Income W2 Employees |

| Traditional Envelope Method | High | Low | High | Very Low | Cash-Based Local Workers |

| No-Budget Tracking System | Very Low | Low | Very High | Medium | Wealthy High-Net-Worth Individuals |

| 70/20/10 High Inflation Layout | Medium | Medium | Medium | High | Stretched Households in High-Cost Cities |

The “Ugly Truth” Section

Let’s cut through the standard financial influencer talk. If you read through real user reviews on Reddit or Trustpilot, you quickly learn where this system hits a wall. In an economy with skyrocketing rent and real-world core inflation, fitting your basic survival costs into a clean 50% box can feel nearly impossible if you earn under $60,000 a year in a major US metropolitan area. Realistically, your housing costs alone might eat up 45% of your income, leaving almost nothing for utilities and groceries.

If you try to force the math blindly, you will end up misclassifying clear lifestyle choices—like expensive delivery apps—as essential “grocery needs” just to make your spreadsheet look good. Don’t play mind games with your finances. If your baseline costs are running too high, own the data, shrink your discretionary spending, and seek out high-leverage remote work opportunities to aggressively boost your top-line revenue.

Step-by-Step Launch Summary Checklist

- [ ] Pull your actual net take-home pay records from the past 90 days across all bank statements.

- [ ] Connect your primary checking accounts to a modern aggregator app using the secure Plaid API.

- [ ] Open a high-yield savings account (HYSA) to serve as your dedicated 20% savings vault.

- [ ] Program your banking app to automatically route 30% of your income to a separate checking account on payday.

- [ ] Set up an automated recurring transfer to send 20% of your net income straight to your high-yield savings vault.

- [ ] Audit your automated categorization filters every 30 days to catch and fix any misclassified transactions.

Disclaimers

Your results may vary. All financial frameworks, automation strategies, and cash flow architectures presented here are for educational purposes only. This information does not constitute formal investment, legal, or licensed financial planning advice. Please consult a certified public accountant (CPA) or a fiduciary financial advisor before deploying advanced capital allocations.

Internal & External Linking Hub

- How to Make Money with Airbnb in 2026 USA Without Owning Property

- Best Work From Home Jobs for Introverts in the USA 2026 (No Phone, No Sales)

- Zero-Based Budgeting 2026 USA

- Best Budgeting Apps USA 2026

- Highest Paying Gig Economy Jobs in the USA 2026

- How to Start a Notion Template Business in 2026 USA

- Freelance Digital Skills That Pay 2026 USA

- Best Budgeting Tips for 2026 in USA

- Voiceover Jobs 2026 USA

- Virtual Bookkeeping Business 2026 USA

- Proofreading Jobs Online 2026 USA

- AI Data Annotation Jobs 2026 USA

- Online Transcription Jobs 2026 USA

- User Testing Jobs 2026 USA

- How to Become an AI Prompt Engineer in 2026 USA

- Best Secret Remote Job Boards 2026 USA

- Upwork for Beginners in 2026 USA

- Pinterest Affiliate Marketing in 2026 USA

- How to Start a Faceless YouTube Channel in 2026 USA

- How to Start Amazon KDP in 2026 USA

- How to Start Dropshipping in 2026 USA

- How to Create and Sell Online Courses in 2026 USA

External Reference Profiles for Verification:

- Bureau of Labor Statistics (BLS)

- Consumer Financial Protection Bureau (CFPB) Budgeting Tools

- IRS Self-Employment Tax Guide

Short FAQ Block

- What if an emergency hits and my 50% needs account runs completely dry? If an unexpected expense comes up, pause your 30% lifestyle spending immediately to free up cash flow, or pull money directly from your emergency savings vault. Do not let your core checking account drop below zero.

- How do I handle unpredictable utility spikes or seasonal heating bills? Look at your total utility costs over the past year, figure out the monthly average, and build that fixed baseline amount right into your monthly 50% needs budget.

- Should I stop saving my 20% if I am focused on paying off student loans? Keep a small, baseline emergency fund in place first. Once that safety net is built, you can aggressively route your entire 20% savings allocation toward wiping out your loan principal.