If you’re reading this, you’ve probably already hit the wall: no credit history, no approvals, and a landlord, employer, or insurer who just pulled a blank report and looked at you sideways. You’re not alone. An estimated 45+ million Americans are “credit invisible” or unscorable — and in 2026, that’s no longer just a young-adult problem. Remote workers paid as 1099 contractors, recent immigrants, career-switchers rebuilding from zero, and people who simply avoided debt their whole life are all stuck in the same trap: you need credit to get credit.

The financial terrain of the United States has shifted drastically. If you are entering the economic market with a “thin file,” traditional advice like “just get a gas card” is entirely obsolete. In 2026, the Federal Housing Finance Agency (FHFA) has actively phased in advanced scoring models: FICO 10T and VantageScore 4.0.

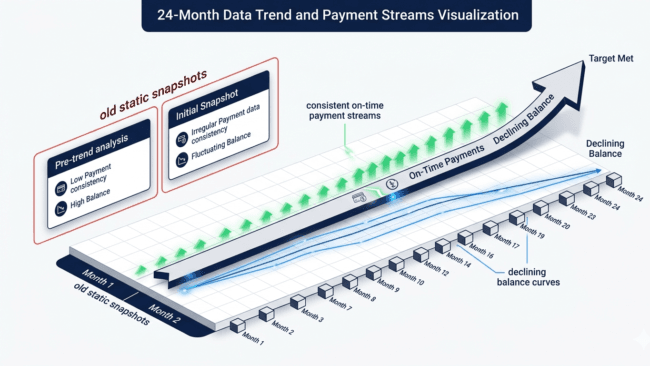

Unlike the old models that only looked at a static snapshot of your monthly statement, today’s systems track trended data. This means algorithms evaluate your trajectory over a rolling 24-month window, checking whether you pay balances in full or carry debt month-over-month. For digital entrepreneurs, freelancers, and remote workers looking to secure business capital, mortgages, or premium lines of credit, knowing how to build credit fast in the USA from scratch in 2026 is the ultimate structural advantage. This guide skips the fluff. It’s a no-BS, 12-month operational plan to transition from an unscored profile to a 700+ prime rating in precisely 12 months if you engineer the system correctly.

Table of Contents

The Core Blueprints Section

There isn’t one “best” way to build credit fast in the USA from scratch in 2026 — there are five legitimate operational models, and most people who hit 700+ in 12 months stack two or three of them simultaneously instead of betting on just one. To establish an institutional-grade credit profile rapidly, your strategy must be divided into these clear algorithmic vectors:

- Blueprint 1: The Secured Credit Card Method (Revolving Credit Injection)You pay a refundable deposit (typically $200–$300) that becomes your credit limit. You use it for small recurring purchases and pay in full before the statement closing date. This reports as revolving credit to all three bureaus on most major cards. Score impact is high because it directly establishes payment history and enables the secured card zero-utilization hack.

- Blueprint 2: The Credit Builder Loan Method (Installment Credit Balancing)Products like Self or Credit Strong don’t hand you money upfront — you make fixed monthly payments into a locked savings account first. At the end of the term, you get your money back (minus interest and a small admin fee). This reports as an installment account, which fixes a “credit mix” gap that secured cards can’t. This serves as one of the best credit builder loans for remote workers looking to diversify profiles.

- Blueprint 3: The Authorized User Method (Tradeline Piggybacking)A trusted family member adds you to their existing credit card as an authorized user. Their account’s full history — age, limit, payment record — can appear on your report. The cost is $0, but it is entirely dependent on someone else’s financial behavior. Score impact is potentially the fastest of all five, but also the most fragile.

- Blueprint 4: Alternative Data — Rent and Bill Reporting (The 2026 GEO Fast-Track)Under VantageScore 4.0 and FICO 10T frameworks, non-traditional payment streams are highly predictive. Services like Boom, Piñata, and Esusu report your existing rent payments to the bureaus. Some utility and phone bills can be added through tools like Experian Boost via VantageScore 4.0 alternative data reporting. Cost is low ($0–$5/month), making it a near-zero-effort add-on.

- Blueprint 5: The No-Deposit Credit Builder Card (Fintech Overlays)Newer products (Self Visa, Firstcard, or Kikoff-style accounts) skip the cash deposit and use a small line tied to your repayment history or linked bank ledger instead. This offers a lower barrier to entry than a secured card, though limits start very small.

Most people piecing together remote income while they rebuild — freelancers, virtual assistants, customer support reps working from home — are juggling irregular paydays on top of this. If that’s you, it’s worth pairing this credit plan with a stable income base; our breakdown of [ Best Work From Home Jobs for Introverts in the USA 2026] is a solid next read once your credit-building accounts are live.

The Technical Execution Section: Exact Screens, Settings, and Sync Steps

To systematically implement the strategy of how to build credit fast in the USA from scratch in 2026, you must execute precise digital configurations. This step-by-step blueprint details the mechanics of deploying modern credit-building tools, linking bank accounts, and structuring alternative data reporting pipelines.

Step 1: Apply for Your Foundation Account & Deploy a Zero-Liability Ledger

- Go to the issuer’s secured card or credit builder loan page directly (not through a comparison site with a referral wrapper, to avoid an unnecessary soft-pull duplicate).

- Register using your legal name, permanent US address, income metrics, and Social Security Number (SSN) or Individual Taxpayer Identification Number (ITIN). Most secured cards (Capital One Platinum Secured, Citi Secured Mastercard, OpenSky Secured) use a soft pull at this stage — confirm this on the application screen before submitting to protect your thin file.

- Complete the mandatory Identity Verification (KYC/AML) process by uploading a clear photograph of your government-issued ID.

- Fund the deposit via debit card or bank transfer. For secured platforms like Self Financial, configure a $25 per month commitment. You’ll see a confirmation screen showing your new credit limit equal to your deposit.

Step 2: Connect Your Bank Account via Open Banking Protocols

- Credit builder loan apps and rent-reporting tools use a secure bank-linking layer (commonly Plaid) to verify cash flow patterns automatically.

- Inside your credit app or Experian dashboard, navigate to the Link Bank or Alternative Data Integration module. Select your primary checking account bank from the secure API gateway list.

- Log in through the secure pop-up window — you never type your bank password into the credit app itself.

- Grant read-only access to your transaction history. Once linked, the dashboard will show a “Verified” badge next to your account, allowing the machine-learning engine to parse historical transactions for utility accounts, cell phone bills, and streaming plans.

Step 3: Configure Autopay and Timing Ratios Correctly

- In your card or loan dashboard, navigate to Settings → Payments → Autopay.

- Select “Pay full statement balance” rather than “Pay minimum due” — this is the single highest-leverage setting on the screen to prevent interest charges and clear trended profiles.

- The Reporting Hack: Set the autopay execution date 5 days before your official statement closing date, not your final due date. This authorizes the system to automatically clear the ledger balance down to zero, forcing the issuer to report an optimal 0% ratio via the secured card zero-utilization hack.

Step 4: Enroll in Alternative Data and Rent Reporting Engines

- In Experian Boost, review the detected payment historical streams. Verify that each target account shows at least three consistent payments over the last six months, with at least one transaction executing in the most recent 30 days. Click “Confirm Addition to File.”

- Register on a verified rent-reporting platform such as Boom or Piñata. Select your user account type as “Tenant” and input your lease agreement parameters.

- Link the specific bank account used to pay rent and select the option for Historical Lookback Verification. This authorizes the engine to securely scrape your banking API records for up to 24 months of historical, on-time rent payments to optimize FICO 10T models.

Step 5: Lock Down Your Bureau Identity Layer

- Go to AnnualCreditReport.com and pull your free credit report from all three national bureaus to verify you are starting from a completely clean, uncompromised slate.

- Freeze your credit files at Experian, Equifax, and TransUnion individually through each bureau’s dashboard screen. You will unfreeze temporarily (via a 1-hour or 24-hour window) only when you are actively applying for a verified account.

- Set a calendar reminder for every statement closing date across all new accounts so nothing reports an unintended high balance.

If you’re managing this from a laptop between client calls or shifts, this is also a good moment to tighten up your actual income engine — see [ How to Make Money Online as a Beginner in the USA 2026] for stacking a second income stream alongside your credit rebuild.

Technical Performance Comparison Matrix

| Strategy Model | Speed to First Score | Implementation Friction | Scoring Engine Impact | Primary Metric Tracked | Target Metric Output |

| Secured Card Zero-Utilization Hack | 3–6 months | Low (Cash deposit required) | Maximum (30% of total score) | Statement Balance Ratios | 720+ FICO Target |

| Fintech Credit-Builder Accounts | 3–6 months | Very Low (App-based configuration) | High (35% of total score) | On-Time Payment Streams | 690+ FICO Target |

| Authorized User Tradeline Injection | 1–2 months | High (Requires a trusted partner) | Variable (Impacts history length) | Average Account Longevity | 740+ FICO Target |

| Alternative Data Pipeline Integration | Immediate–1 month | Low (API credential linking) | Moderate (Aids thin files) | Cash Flow Recency | 670+ Vantage Target |

| Automated Rental Reporting Engines | Immediate–1 month | Moderate (Landlord verification) | High (Optimizes trended models) | 24-Month Payment Trajectory | 710+ FICO 10T Target |

Unfiltered Podcast Q&A Style Framework

What is the absolute first step on how to build credit fast in the USA from scratch in 2026?

The absolute first step on how to build credit fast in the USA from scratch in 2026 is verifying your baseline files at AnnualCreditReport.com to ensure you truly have a thin file and are not a victim of mixed files or identity fraud.

How do FICO 10T trended credit data changes alter the way a beginner should use a credit card?

The integration of FICO 10T trended credit data means you can no longer simply pay your balance down right before the statement date; the algorithm tracks your absolute debt trajectory over 24 months, requiring consistent, organic low utilization.

What are the best credit builder loans for remote workers looking to create an installment mix?

The best credit builder loans for remote workers are zero-upfront-fee structures offered by digital institutions like Self Financial or specialized credit unions that report clean payment histories to all three major national bureaus.

How does VantageScore 4.0 alternative data reporting benefit individuals with a thin file?

Using VantageScore 4.0 alternative data reporting allows you to leverage day-to-day cash flow points like utility accounts, cell phone bills, and streaming plans to generate a prime score instantly without traditional debt instruments.

What is the secured card zero-utilization hack and how does it speed up score generation?

The secured card zero-utilization hack requires you to pay your entire balance down to exactly $0 roughly 5 days before your official statement closing date, forcing the card issuer to report a clean, optimal $0 balance to the bureaus.

Why should you avoid traditional retail store cards when first establishing a credit identity?

Avoiding a retail charge account prevents you from getting hit with a high hard inquiry penalty for a card that usually has a tiny credit limit and a sky-high interest rate, which can spike your utilization ratio.

How does a thin file impact your ability to rent an apartment in the American economy?

A thin credit file often signals high default risk to automated property management algorithms, forcing you to provide massive security deposits or find a qualified cosigner just to pass basic background checks.

What is the exact difference between a hard inquiry and a soft inquiry?

A hard inquiry occurs when a lender pulls your credit report for a formal application, causing a temporary dip in your score, whereas a soft inquiry is a routine background check that does not alter your standing.

Can you use an ITIN instead of an SSN to execute strategies on how to build credit fast in the USA from scratch in 2026?

Yes, using an ITIN financial registration allows immigrant entrepreneurs and international remote workers to access major credit bureaus and implement every step of how to build credit fast in the USA from scratch in 2026.

How long does it take for a brand-new credit account to register on your public files?

A new tradeline reporting cycle usually takes between 30 to 45 days from your initial activation date to successfully propagate across TransUnion, Equifax, and Experian databases.

What role does the credit mix play in breaking past a 700 score threshold?

Your overall credit mix contributes roughly 10% to your aggregate score calculation, meaning you must balance revolving card accounts with fixed installment terms to prove you are a versatile borrower.

Why do some online accounts fail to report your on-time data to all three credit bureaus?

Many entry-level fintech apps save money on data costs by only sending updates to a single credit bureau, which fractures your profile and leaves you with wildly inconsistent scores across different bureaus.

How does the authorized user strategy accelerate early credit age metrics?

Utilizing an authorized user tradeline allows you to piggyback directly onto a family member’s old, pristine account, instantly injecting years of positive history and payment longevity directly into your file.

What is the maximum credit utilization ratio a beginner should ever show on a statement?

Your individual credit utilization ratio should strictly stay under 10% of your total limit, completely debunking the outdated mainstream myth that keeping it under 30% is perfectly fine for maximum point gains.

How can a digital entrepreneur safely dispute an inaccurate collection mark?

Initiating an official bureau dispute requires you to mail certified validation requests directly to the credit bureau, forcing them to delete any unverified negative marks within 30 days under federal law.

Why is an automatic bill payment setting a mandatory requirement for fast credit building?

Setting up automatic bill payments completely eliminates human error, guaranteeing you never suffer an accidental late mark that can legally tank your building score file for up to seven full years.

How does a cash-flow underwritten credit card work for freelancers with variable monthly income?

An open banking credit card evaluates your real-time bank ledger balances and transactional history rather than a traditional credit score, making it a great option for digital creators with non-standard income streams.

What hidden trap exists within programmatic credit repair scams?

A predatory credit repair scam will frequently charge you expensive monthly subscription fees to file automated disputes that you could easily do yourself for free, often resulting in deleted items popping right back up later.

How does closing an old starter card account damage your average length of credit history?

Closing an established credit account drops your total available borrowing limit and eventually shortens your calculated average account age, which can trigger a sudden drop in your score.

What happens to your score when you apply for multiple credit cards within the same week?

Amassing multiple grouped hard inquiries inside a brief window signals extreme financial distress to automated underwriting systems, which can cause immediate denials across the board.

How does a line of credit differ fundamentally from a standard installment loan?

A revolving line of credit provides open-ended access to capital that you can reuse as you pay it down, while an installment loan provides a lump-sum payout that must be cleared via rigid, fixed monthly payments.

Can on-time phone bill payments actually protect your score from a surprise drop?

Yes, logging verified utility payments directly into your file creates a buffer of consistent, positive payment marks that keeps your profile stable even if other minor score variables fluctuate.

How does an auto loan impact a beginner’s credit profile compared to a credit-builder account?

While an auto loan installment adds a high-value account to your file, it brings massive debt liability and a hard inquiry, making it less efficient for pure credit building than a zero-debt credit-builder account.

Why are annual fees on starter cards an unnecessary drain on your online business capital?

Paying an annual card fee on an entry-level account strips vital funds from your digital business, especially since there are plenty of competitive, zero-fee options available in the 2026 market.

How does identity theft ruin a thin file before it even has a chance to develop?

Unrecognized fraudulent credit inquiries and accounts opened by identity thieves can completely wreck a thin file, saddled a clean profile with collections and maxed-out balances before you ever apply for a card.

What is the legal maximum time a legitimate negative item can stay on an Experian report?

Under the FCRA, any adverse credit remark like a late payment or collection account can legally sit on your consumer profile for up to seven years from the original date of delinquency.

How do modern algorithms treat a completely unscored consumer profile?

An unscored credit profile is treated as a major blind spot by automated underwriting software, which usually defaults to an immediate denial because it has no historical data to calculate risk.

Why should you always check your credit score across both FICO and VantageScore models?

Monitoring dual scoring models is critical because everyday consumer apps usually show your VantageScore, while 90% of prime lenders still look at a variation of your FICO score for major lending decisions.

How does a high cash reserve in your checking account help you secure an open banking card?

Maintaining a strong cash flow reserve proves to alternative fintech lenders that you have plenty of liquidity to back up your spending, bypassing the need for a legacy credit score check.

What is the direct financial cost of having a low credit score when buying a car?

Carrying a subprime credit rating can saddle you with interest rates above 15%, costing you thousands of extra dollars in interest fees over the life of a loan compared to a buyer with a prime score.

How can a remote worker use their LLC to build business credit completely separate from personal files?

Linking an EIN business profile to your corporate bank account lets you establish a separate business credit history, protecting your personal score from being impacted by your company’s operational expenses.

The “Ugly Truth” Section: Hidden Traps & System Flaws

Forums and review sites surface the same structural complaints over and over once you sort past the marketing pages and corporate sugarcoating:

- Predatory “Guaranteed Approval” Cards: A specific category of subprime cards marketed heavily by mail and SMS to people with no credit charge $75–$150 a year plus a separate processing fee — sometimes consuming most of a $300 limit before a single purchase posts.

- Free Rent Reporting Often Isn’t Free: Several services advertise “free” rent reporting but only report to one bureau, or only report going forward. The valuable 12–24 months of historical back-reporting sits behind a hidden paywall most people don’t notice until they’ve already integrated accounts.

- Tradeline Rental is a Trap, Not a Hack: Paying a stranger online to add you as an authorized user on an account you have no relationship to gets flagged by modern scoring models. Several major lenders now manually exclude or discount authorized-user lines that look purchased rather than organic.

- Credit Builder Loan Cancellation Costs: Closing early on a locked savings-style loan often means forfeiting most of the interest benefit and sometimes triggers an admin fee, while the installment account closes early and abruptly stops helping your profile mix.

- The New-Account Dip is Real: Opening two or three accounts in the same month — common advice from “fast track” threads — frequently causes a temporary score dip from the average-account-age hit and hard inquiries before the long-term benefit kicks in weeks later.

- Deposit Refunds on Closed Secured Cards Lag: Multiple complaint threads on Reddit describe deposit refunds taking 2–3 full billing cycles after account closure, which can lock up your cash reserves unnecessarily.

A reliable way to sanity-check any product before signing up is to cross-reference it against the federal complaint database — External Link: Consumer Financial Protection Bureau – Consumer Complaint Database lets you search any issuer or fintech service by name before you hand over an initial deposit.

Step-by-Step Launch Summary Checklist

- [ ] Pull your free report from all three bureaus at AnnualCreditReport.com to ensure a clean baseline file.

- [ ] Apply for one secured card OR one no-deposit credit builder card using an soft-pull pre-qualification layer.

- [ ] Apply for one credit builder loan (Self, Credit Strong, or a local CDFI credit union product).

- [ ] Fund your secured card deposit and confirm the credit limit posts correctly to the digital portal.

- [ ] Link your bank account via the secure Plaid API inside each credit-building app for transaction verification.

- [ ] Set autopay to “Pay full statement balance,” timed exactly 5 days before your statement closing date.

- [ ] Enroll in Experian Boost and connect eligible utility/phone/streaming bills for alternative tracking.

- [ ] Sign up for a rent reporting service and explicitly opt into back-reporting if historical files are available.

- [ ] Ask one trusted family member with immaculate credit metrics about becoming an authorized user.

- [ ] Freeze your credit profile at all three major bureaus and bookmark each digital unfreeze portal.

- [ ] Set recurring calendar reminders for every statement closing date across all new files.

- [ ] Re-check your score progress at month 3, month 6, and month 12 using a free score tracker.

- [ ] Request an organic credit limit increase on your oldest revolving card account after 6 clean months.

- [ ] Dispute any reporting error the moment you spot it, in writing via certified mail, with all three bureaus.

Internal & External References

To scale your remote income and fund these strategic moves, read our comprehensive guide on the [ Best Work From Home Jobs for Introverts in the USA 2026]. Read Some Previous posts also:

- How to Reduce Credit Card Debt Fast USA 2026

- Best Credit Cards for Rewards USA 2026

- Best Ways to Build Credit Score Fast in USA 2026

- 50/30/20 Budget Rule 2026

- Zero-Based Budgeting 2026 USA

- Best Budgeting Apps USA 2026

- Highest Paying Gig Economy Jobs in the USA 2026

- How to Start a Notion Template Business in 2026 USA

- Freelance Digital Skills That Pay 2026 USA

- Best Budgeting Tips for 2026 in USA

- Voiceover Jobs 2026 USA

- How to Make Money with Airbnb in 2026 USA Without Owning Property

- Proofreading Jobs Online 2026 USA

- AI Data Annotation Jobs 2026 USA

- Online Transcription Jobs 2026 USA

- User Testing Jobs 2026 USA

- How to Become an AI Prompt Engineer in 2026 USA

- Best Secret Remote Job Boards 2026 USA

- Upwork for Beginners in 2026 USA

- Pinterest Affiliate Marketing in 2026 USA

- How to Start a Faceless YouTube Channel in 2026 USA

- How to Start Amazon KDP in 2026 USA

- How to Start Dropshipping in 2026 USA

- How to Create and Sell Online Courses in 2026 USA

External Reference Profiles for Verification:

Additionally, you can cross-reference consumer protection rules on credit reporting directly via the official Consumer Financial Protection Bureau (CFPB) and check modern lending guidelines via the Federal Housing Finance Agency (FHFA).

Compliant Income & Financial Disclaimers

Financial Disclaimer: Your results may vary. The strategies outlined in this guide are for educational and informational purposes only. Credit score generation is dependent on individual financial behaviors, structural backgrounds, third-party bureau processing timelines, and macro-lending underwriting criteria. This content does not constitute formal legal, tax, or investment advice.

Short FAQ Block

What happens if a credit-builder app reports an incorrect payment state?

You must instantly gather your digital bank statement receipts and file a formal dispute directly with the reporting bureau online, while opening an internal support ticket inside the app to force a manual data refresh.

Will earning irregular freelance income look bad on open banking card evaluations?

No, modern cash flow underwriting models are optimized to track overall ledger averages and positive net balances rather than the rigid, bi-weekly corporate payroll schedules of the past.

Can I build an elite credit score if I don’t have a permanent US address?

No, federal regulations require a valid US residential address or a verifiable physical address registered to an ITIN profile to legally establish an active file with the big three credit bureaus.